When it comes to planning for your retirement income, it’s easy to overlook some of the common factors that can affect how much you’ll have available to spend. If you don’t consider how your retirement income can be impacted by investment risk, inflation risk, catastrophic illness or long-term care, and taxes, you may not be able to enjoy the retirement you envision.

Investment risk

Different types of investments carry with them different risks. Sound retirement income planning involves understanding these risks and how they can influence your available income in retirement.

Investment or market risk is the risk that fluctuations in the securities market may result in the reduction and/or depletion of the value of your retirement savings. If you need to wi

thdraw from your investments to supplement your retirement income, two important factors in determining how long your investments will last are the amount of the withdrawals you take and the growth and/or earnings your investments experience. You might base the anticipated rate of return of your investments on the presumption that market fluctuations will average out over time, and estimate how long your savings will last based on an anticipated, average rate of return.

Unfortunately, the market doesn’t always generate positive returns. Sometimes there are periods lasting

for a few years or longer when the market provides negative returns. During these periods, constant withdrawals from your savings combined with prolonged negative market returns can result in the depletion of your savings far sooner than planned.

Reinvestment risk is the risk that proceeds available for reinvestment must be reinvested at an interest rate that’s lower than the rate of the instrument that generated the proceeds. This could mean that you have to reinvest at a lower rate of return, or take on additional risk to achieve the same level of return. This type of risk is often associated with fixed interest savings instruments such as bonds or bank certificates of deposit. When the instrument matures, comparable instruments may not be paying the same return or a better return as the matured investment.

Interest rate risk occurs when interest rates rise and the prices of some existing investments drop. For example, during periods of rising interest rates, newer bond issues will likely yield higher coupon rates than older bonds issued during periods of lower interest rates, thus decreasing the market value of the older bonds. You also might see the market value of some stocks and mutual funds drop due to interest rate hikes because some investors will shift their money from these stocks and mutual funds to lower-risk fixed investments paying higher interest rates compared to prior years.

Inflation risk

Inflation is the risk that the purchasing power of a dollar

will decline over time, due to the rising cost of goods and services. If inflation runs at its historical long term average of about 3%, the purchasing power of a given sum of money will be cut in half in 23 years. If it jumps to 4%, the purchasing power is cut in half in 18 years.

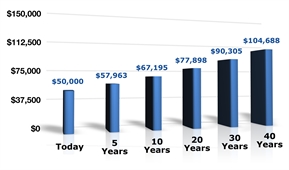

A simple example illustrates the impact of inflation on retirement income. Assuming a consistent annual inflation rate of 3%, and excluding taxes and investment returns in general, if $50,000 satisfies your retirement income needs this year, you’ll need $51,500 of income next year to meet the same income needs. In 10 years, you’ll need about $67,195 to equal the purchasing power of $50,000 this year. Therefore, to outpace inflation, you should try to have some strategy in place that allows your income stream to grow throughout retirement.

(The following hypothetical example is for illustrative purposes only and assumes a 3% annual rate of inflation without considering taxes. It does not reflect the performance of any particular investment.)

Equivalent Purchasing Power of $50,000 at 3% Inflation

Long-term care expenses

Long-term care may be needed when physical or mental disabilities impair your capacity to perform everyday basic tasks. As life expectancies increase, so does the potential need for long-term care.

Paying for long-term care can have a significant impact on retirement income and savings, especially for the healthy spouse. While not everyone needs long-term care during their lives, ignoring the possibility of such care and failing to plan for it can leave you or your spouse with little or no income or savings if such care is needed. Even if you decide to buy long-term care insurance, don’t forget to factor the premium cost into your retirement income needs.

The costs of catastrophic care

As the number of employers providing retirement health-care benefits dwindles and the cost of medical care continues to spiral upward, planning for catastrophic health-care costs in retirement is becoming more important. If you recently retired from a job that provided health insurance, you may not fully appreciate how much health care really costs.

Despite the availability of Medicare coverage, you’ll likely have to pay for additional health-related expenses out-of-pocket. You may have to pay the rising premium costs of Medicare optional Part B coverage (which helps pay for outpatient services) and/or Part D prescription drug coverage. You may also want to buy supplemental Medigap insurance, which is used to pay Medicare deductibles and co-payments and to provide protection against catastrophic expenses that either exceed Medicare benefits or are not covered by Medicare at all. Otherwise, you may need to cover Medicare deductibles, co-payments, and other costs out-of-pocket.

Taxes

The effect of taxes on your retirement savings and income is an often overlooked but significant aspect of retirement income planning. Taxes can eat into your income, significantly reducing the amount you have available to spend in retirement.

It’s important to understand how your investments are taxed. Some income, like interest, is taxed at ordinary income tax rates. Other income, like long-term capital gains and qualifying dividends, currently benefit from special–generally lower–maximum tax rates. Some specific investments, like certain municipal bonds, generate income that is exempt from federal income tax altogether. You should understand how the income generated by your investments is taxed, so that you can factor the tax into your overall projection.

Taxes can impact your available retirement income, especially if a significant portion of your savings and/or income comes from tax-qualified accounts such as pensions, 401(k)s, and traditional IRAs, since most, if not all, of the income from these accounts is subject to income taxes. Understanding the tax consequences of these investments is vital when making retirement income projections.

Have you planned for these factors?

When planning for your retirement, consider these common factors that can affect your income and savings. While many of these same issues can affect your income during your working years, you may not notice their influence because you’re not depending on your savings as a major source of income. However, investment risk, inflation, taxes, and health-related expenses can greatly affect your retirement income.

IMPORTANT DISCLOSURES

Altum Wealth Advisors does not provide investment, tax, or legal advice via this website. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

CIRCULAR 230 NOTICE: To ensure compliance with requirements imposed by the IRS, this notice is to inform you that any tax advice included in this communication, including any attachments, is not intended or written to be used, and cannot be used, for the purpose of avoiding any federal tax penalty or promoting, marketing, or recommending to another party any transaction or matter.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2014.

Prepared for Altum Wealth Advisors, Steven Cliadakis, MBA, CWS®, Managing Director, Wealth Strategist. Chico, CA, San Francisco, CA.